Stabilization Is Not Resilience: Why Income Logic Needs Infrastructure

Defect rates have stabilized.

The ACES Q3 2025 report placed the critical defect rate at 1.79%, up from 1.51% in Q2. After several volatile years, that feels like normalization.

But in mortgage lending, stable averages can hide a different problem: concentration risk.

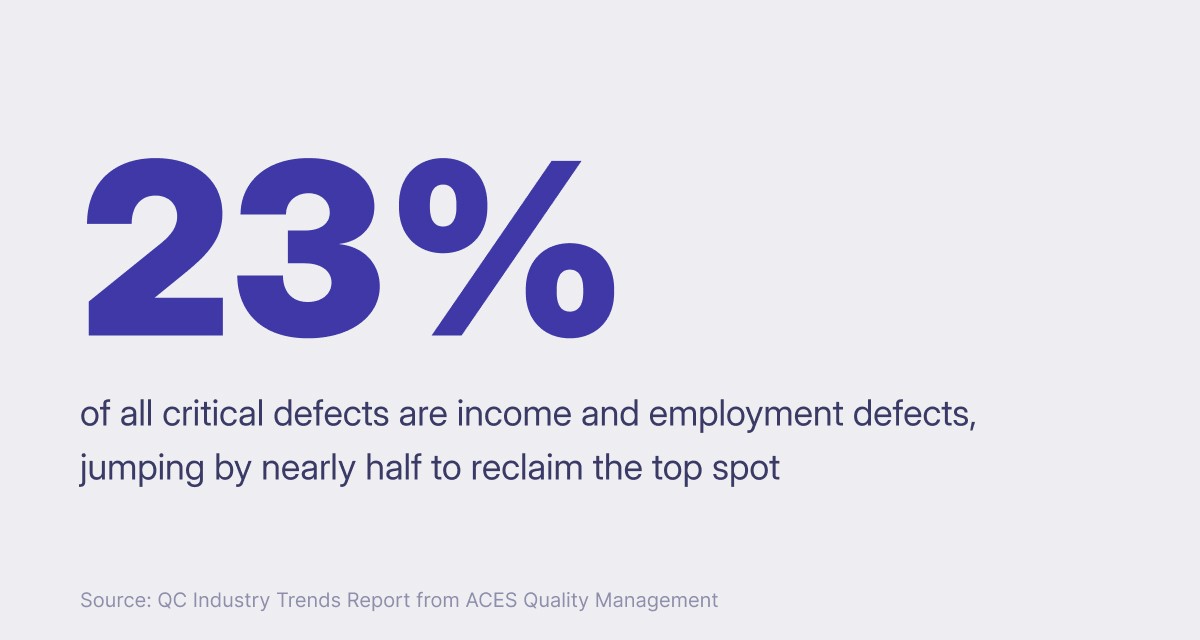

In the same study, income and employment defects now account for more than 20% of all critical findings. In other words, nearly a quarter of total defect exposure is concentrated in a single category, which may be pointing to a deeper operational challenge in your pipeline.

Where Income Logic Lives

Income is rarely calculated once. It is recalculated as files move between products, investors change, borrowers add co-applicants, or continuity is questioned. Each recalculation introduces the possibility of interpretive drift.

Now layer in staffing dynamics. Your experienced underwriters retire. Your teams expand or shift. Institutional knowledge becomes uneven.

As income calculations move across products, investors, and underwriting teams, interpretation inevitably begins to drift.

That variability helps explain the 23% concentration.

Income logic often lives in memory, pattern recognition, and personal familiarity with edge cases. When that logic is not institutionalized, the organization does not fully own it.

And when judgment-heavy analysis is repeatedly reconstructed without shared infrastructure, defect concentration becomes predictable.

Your QC team can measure that variability. They cannot eliminate it.

Our Structural Response: Upfront Income

The challenge is not simply calculating income. It is maintaining a consistent analysis as a loan evolves. Documentation changes, borrowers add income sources, and program eligibility shifts. A single file may involve W-2 wages, rental properties, partnerships, self-employment, or layered ownership structures.

Managing that complexity requires a single place where income can be structured, calculated, and updated as the file changes.

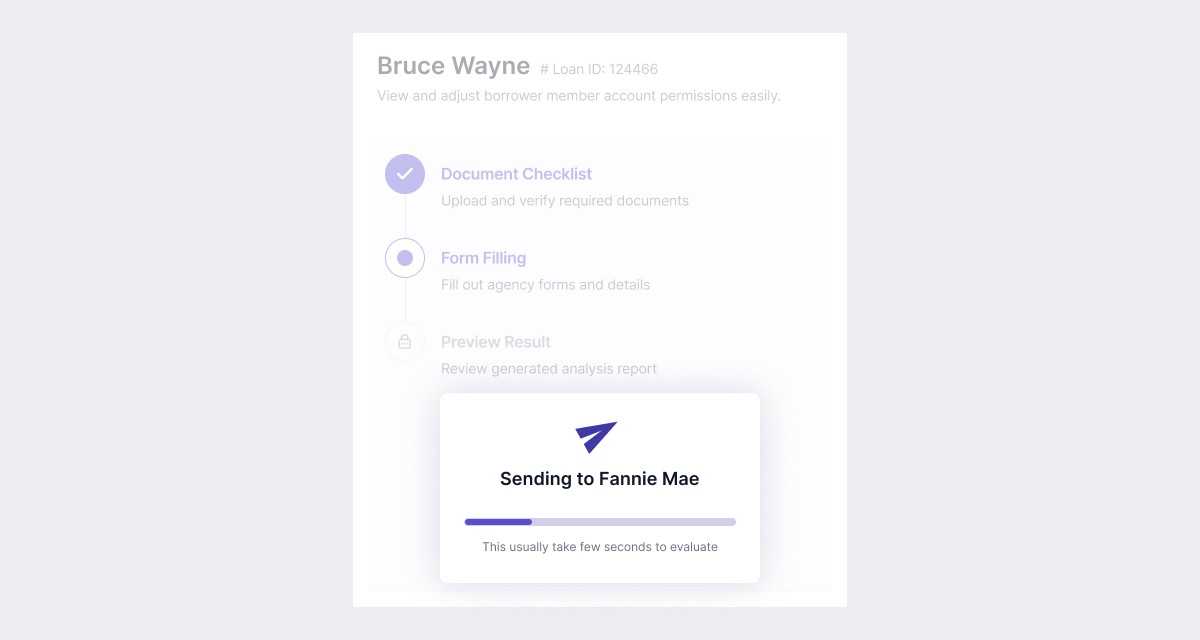

Upfront Income gives your team that platform across both QM and Non-QM workflows, creating a continuous income analysis without the need to restart calculations across multiple systems.

One continuous workflow for the entire loan lifecycle

When your loan officers upload income documents, the platform structures the file, and Qualified Income is calculated automatically based on the available documentation.

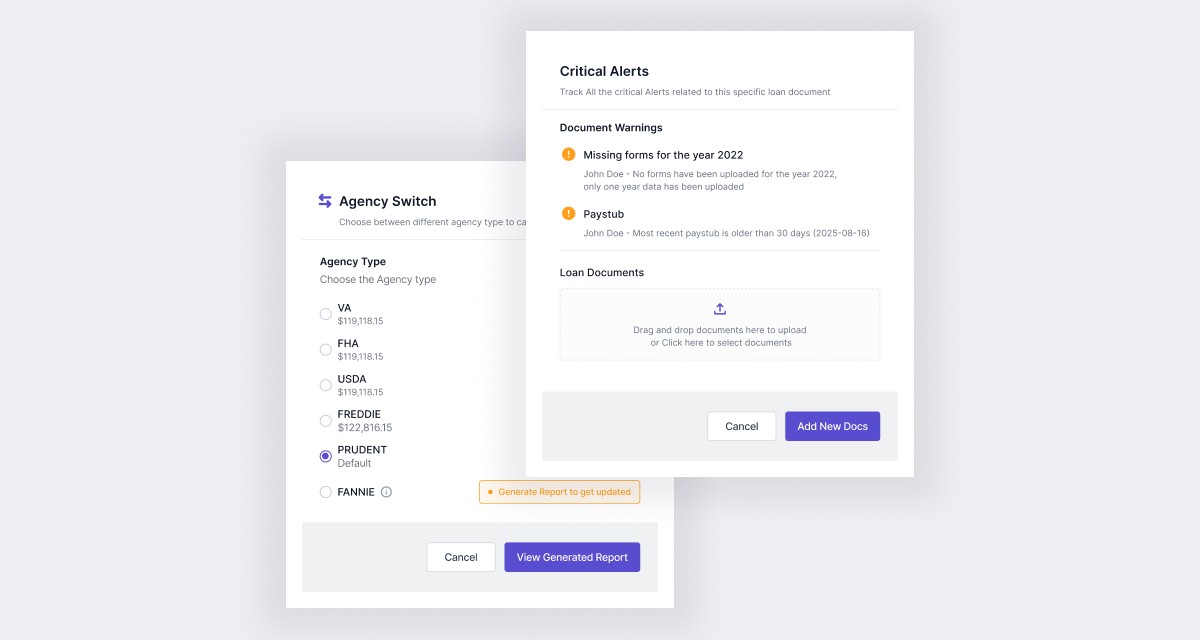

With income organized and calculated in one place, your staff can evaluate how the borrower qualifies under different agency guidelines, including VA, FHA, USDA, Freddie Mac, or Fannie Mae, without rebuilding the income analysis each time.

For lenders working with agency loans, Upfront Income also integrates directly with Fannie Mae Self-Employed and Rental Income Calculators. This means there is no need to switch tools or re-enter data. Calculations follow agency guidelines automatically using the same structured income data without reinterpreting again and again.

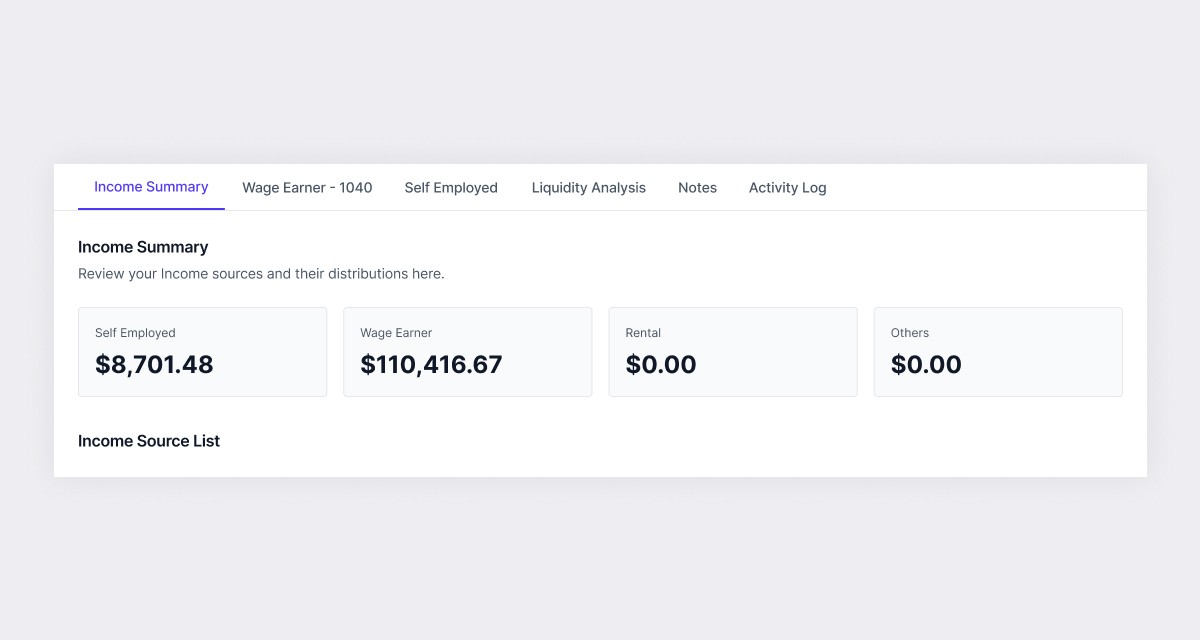

The key benefit is continuity. As the file evolves, documents can be added or excluded, assumptions can be adjusted, and different program requirements can be applied while the same structured income data stays attached to the loan. The analysis moves forward with the file rather than being recalculated from scratch.

This creates a consistent income record from intake through underwriting and secondary review, reducing interpretive drift and helping your underwriters and loan officers arrive at the same Qualified Income conclusion regardless of who touches the file.

This is not yet another tool

Upfront Income is designed to fit into the way your teams already work.

Through a Self-Serve Portal, brokers and loan officers upload documents directly and your team receives complete, decision-ready files from the start. This reduces follow-ups and eliminates the back-and-forth of documents trickling in piece by piece — cutting down the number of touches for everyone involved.

Through APIs, Upfront Income connects directly to LOS tools like Encompass and your POS, triggering income analysis automatically and pushing structured results back into your existing workflow.

And with Plaid, verified balances, transactions, and cash flow are pulled in automatically, so your team is no longer dependent on the borrower to provide bank documents manually.

Stability Is Not the Finish Line

If income remains the largest concentration of defect exposure in a stabilized market, it's also where the greatest opportunity for improvement sits. Adding more reviewers and review cycles addresses the output, not the process that produced it.

The real shift is building consistent logic into the workflow itself. Upfront Income does that by keeping income analysis structured and continuous from intake through underwriting, so fewer defects are created in the first place. Stability in the averages is a starting point. Structural resilience is when your team's income analysis works as shared infrastructure, not individual judgment.

Defect rates have stabilized.

The ACES Q3 2025 report placed the critical defect rate at 1.79%, up from 1.51% in Q2. After several volatile years, that feels like normalization.

But in mortgage lending, stable averages can hide a different problem: concentration risk.

In the same study, income and employment defects now account for more than 20% of all critical findings. In other words, nearly a quarter of total defect exposure is concentrated in a single category, which may be pointing to a deeper operational challenge in your pipeline.

Where Income Logic Lives

Income is rarely calculated once. It is recalculated as files move between products, investors change, borrowers add co-applicants, or continuity is questioned. Each recalculation introduces the possibility of interpretive drift.

Now layer in staffing dynamics. Your experienced underwriters retire. Your teams expand or shift. Institutional knowledge becomes uneven.

As income calculations move across products, investors, and underwriting teams, interpretation inevitably begins to drift.

That variability helps explain the 23% concentration.

Income logic often lives in memory, pattern recognition, and personal familiarity with edge cases. When that logic is not institutionalized, the organization does not fully own it.

And when judgment-heavy analysis is repeatedly reconstructed without shared infrastructure, defect concentration becomes predictable.

Your QC team can measure that variability. They cannot eliminate it.

Our Structural Response: Upfront Income

The challenge is not simply calculating income. It is maintaining a consistent analysis as a loan evolves. Documentation changes, borrowers add income sources, and program eligibility shifts. A single file may involve W-2 wages, rental properties, partnerships, self-employment, or layered ownership structures.

Managing that complexity requires a single place where income can be structured, calculated, and updated as the file changes.

Upfront Income gives your team that platform across both QM and Non-QM workflows, creating a continuous income analysis without the need to restart calculations across multiple systems.

One continuous workflow for the entire loan lifecycle

When your loan officers upload income documents, the platform structures the file, and Qualified Income is calculated automatically based on the available documentation.

With income organized and calculated in one place, your staff can evaluate how the borrower qualifies under different agency guidelines, including VA, FHA, USDA, Freddie Mac, or Fannie Mae, without rebuilding the income analysis each time.

For lenders working with agency loans, Upfront Income also integrates directly with Fannie Mae Self-Employed and Rental Income Calculators. This means there is no need to switch tools or re-enter data. Calculations follow agency guidelines automatically using the same structured income data without reinterpreting again and again.

The key benefit is continuity. As the file evolves, documents can be added or excluded, assumptions can be adjusted, and different program requirements can be applied while the same structured income data stays attached to the loan. The analysis moves forward with the file rather than being recalculated from scratch.

This creates a consistent income record from intake through underwriting and secondary review, reducing interpretive drift and helping your underwriters and loan officers arrive at the same Qualified Income conclusion regardless of who touches the file.

This is not yet another tool

Upfront Income is designed to fit into the way your teams already work.

Through a Self-Serve Portal, brokers and loan officers upload documents directly and your team receives complete, decision-ready files from the start. This reduces follow-ups and eliminates the back-and-forth of documents trickling in piece by piece — cutting down the number of touches for everyone involved.

Through APIs, Upfront Income connects directly to LOS tools like Encompass and your POS, triggering income analysis automatically and pushing structured results back into your existing workflow.

And with Plaid, verified balances, transactions, and cash flow are pulled in automatically, so your team is no longer dependent on the borrower to provide bank documents manually.

Stability Is Not the Finish Line

If income remains the largest concentration of defect exposure in a stabilized market, it's also where the greatest opportunity for improvement sits. Adding more reviewers and review cycles addresses the output, not the process that produced it.

The real shift is building consistent logic into the workflow itself. Upfront Income does that by keeping income analysis structured and continuous from intake through underwriting, so fewer defects are created in the first place. Stability in the averages is a starting point. Structural resilience is when your team's income analysis works as shared infrastructure, not individual judgment.

Get AI Co-pilots that work across your organization

From loan officers to underwriters, Prudent AI ensures each team member works faster, with less risk, and with confidence in every loan file

Put AI Co-pilots to Work Across your Lending Team

From loan officers to underwriters, Prudent AI ensures each team member works faster, with less risk, and with confidence in every file

Put AI Co-pilots to Work Across your Lending Team

From loan officers to underwriters, Prudent AI ensures each team member works faster, with less risk, and with confidence in every file

Prudent AI is a Pre-underwriting Automation Platform for modern mortgage lenders

Get insights from Mortgage experts, industry predictions, and smart ways to stay ahead of the curve delivered to your inbox—in a simplified way!

Prudent AI is a Pre-underwriting Automation Platform for modern mortgage lenders

Get insights from Mortgage experts, industry predictions, and smart ways to stay ahead of the curve delivered to your inbox—in a simplified way!